It has taken two and a half years but this week the Government finally got around to unveiling the details of its low cost loan scheme to incentivise homeowners to undertake energy retrofits. The scheme was first flagged at the publication of the Climate Action Plan and its associated National Retrofit Plan in November 2021.

Details of the loan scheme were initially promised to be revealed in 2022 by the Minister responsible, Éamon Ryan. That deadline, and at least four successive ones, were all missed. Meanwhile, the pace of domestic retrofits to the B2 Building Energy Rating standard has been lagging well behind the pace required to meet the 2030 target of 500,000 home retrofits, set by the Government.

Part of the problem has been a shortage of contractors to carry out the works but homeowners have also been put off by the potential cost. Back in 2021, Ryan’s Department of the Environment, Climate and Communications estimated that retrofitting a house to a BER B2 level and installing a heat pump would cost between €14,000 and €66,000. As with all such things, those costs have inevitably risen since.

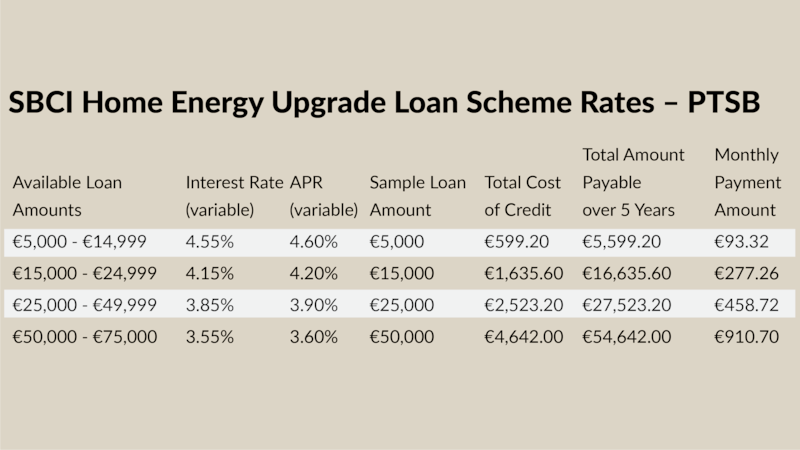

Rising interest rates over that time mean the first offering under the €500 million Home Energy Upgrade Loan Scheme announced on Wednesday is coming in above the 3 per cent to 3.5 per cent promised. .

PTSB has organised funding for the scheme with the Strategic Banking Corporation of Ireland, the State bank whose prime focus is organising affordable funding solutions for Irelands small and medium-sized businesses, at rates varying from 3.55 per cent and 4.55 per cent. The lower the amount borrowed, the higher the interest rate.

We’re assured that other banks will follow PTSB shortly in offering similar low cost borrowing for these SEAI-approved energy retrofits, including AIB, Bank of Ireland and Avant Money, as well as seven credit unions. Each will make their own call on interest rates but it is likely that some will be offering even more attractive rates than PTSB.

So how does it work and who can avail of these loans? And crucially, how do they go about it?

Who qualifies?

It is open to any homeowner, including landlords who can apply in respect of no more than three properties. Companies are excluded, as is anyone applying on behalf of another person. Also excluded are properties used as holiday homes or for short-term Airbnb-type lettings in the previous 12 months. If part of the property has been used for commercial purposes in the past year, it will also be excluded. In all three cases, you’ll need to undertake that you do not carry out any of those activities for at least a year after you secure the funding.

You need to be resident in Ireland. The property you are applying for financial support to retrofit must be located in the Republic and you must prove your ownership of the property by providing its MPRN (electricity meter point reference number). An applicant cannot be either insolvent or bankrupt.

You must also be in receipt of an SEAI grant for the works you are undertaking. That means you have to fulfil the criteria of one of the National Home Energy Upgrade Scheme or the Better Energy Homes Scheme. Details can be found on the grants page of the SEAI website. Most grants apply only to homes built before 2011. Houses seeking heat pumps can be much more recently built. The SEAI site says it can take up to six weeks to finalise grant funding. It could be longer.

How do I apply?

Your first step is to arrange an energy assessment of your property. This must be carried out by one of the one-stop shops approved by the Sustainable Energy Authority of Ireland (SEAI), an SEAI-approved energy partner or a registered community project coordinator and you will pay for it regardless of whether it leads to a successful loan application or not.

If it finds that the proposed upgrades will improve your home’s energy efficiency by 20 per cent or more, you qualify. The approved person you have engaged will manage the process from start to finish and carry out all the works.

You then access one of the loan providers through the SBCI website.

How much can I get?

You can borrow anywhere between €5,000 and €75,000 per property repayable over anything from one to 10 years. An individual applicant can apply for retrofitting on up to three properties with a €225,000 cap on individual borrowing. The money is unsecured which means, unlike a mortgage, the lender has no security, such as your home, against the loan.

The SBCI also says that people can avail of more than one loan as long as the total does not exceed the €75,000 per property / €225,000 per person cap.

When can I access the funds?

The loans are accessible now and will be available until the end of 2026, unless the €500 million allocated for it is fully subscribed for before then. The first provider, PTSB, has access to €100 million of this funding.

What sorts of energy upgrades are covered?

That depends whether you go the Better Energy Homes Scheme route or the National Home Energy Upgrade Scheme via a one-stop shop. Both cover things like wall, roof and attic insulation. That includes insulation of external walls, internal walls or cavity block walls. Heat pumps and heating controls are also covered as is solar water heating.

But if you are looking at new windows, floor insulation, ventilation or installing solar panels, these are only available on the latter scheme.

On the flip side, using the former route does allow you to upgrade on a step-by-step basis as funding or other factors allow. Under the one-stop shop route, the whole upgrade is done at the one time.

Are there any specific rules attached to the funds?

Yes, you need to spend at least three-quarters of the loan on the energy upgrades. The balance can be spent on putting the house right again – painting and so on – after the works have been completed.

Also, you cannot apply for loans for work that has already been completed, so get the grant funding and the paperwork done before you engage anyone to do the work.

How competitive are these rates?

They are certainly competitive compared to PTSB’s current home improvement loan rate of 7.9 per cent, or its personal loan rates which range from 10 per cent to 13.4 per cent.

PTSB’s home improvement rates are not the most competitive but the new low cost loan rate still compares favourably to AIB’s current green loan offer of 6.25 per cent, An Post’s 6.7 per cent or Avant’s 6.9 per cent. What those banks offer under the new low cost loan scheme remains to be seen.

Why are banks offering low rates for these products?

The Government is subsidising the interest rates by two percentage points to allow the bank offerings to be more attractive for homeowners. The banks also have the comfort of a European Investment Bank guarantee which ensures they will recover 80 per cent of their money even if the borrower defaults.

However, if you do not repay the money or use it for purposes other than those agreed, the preferential loan rate will be dropped after three years and you may be charged a higher rate of interest. In those circumstances, the bank can also demand immediate repayment of the full loan.

What’s in it for me?

All sorts of things. First, you have the peace of mind of knowing that you are making your house as energy efficient as possible. Apart from doing your bit to ease our climate change headache, you should also benefit from lower energy bills and, depending on whether you go solar or not, even the change to make some money by selling power back into the grid.

Another practical benefit of improving your home’s building energy rating is that it should allow you to switch your mortgage to a green loan rate which are the most competitive in the market, saving you further money on your monthly bills.

So everybody’s happy?

If my network is anything to go by, a lot of people have put off undertaking significant energy upgrades pending the release of details about these low cost loans, so I would expect it will trigger an acceleration of applications for retrofits.

Commenting on the announcement, Friends of the Earth described it as “welcome”, including its inclusion of small private sector landlords.

“This loan scheme gives households agency to retrofit in stages and at a pace that works for them, taking some pressure off to undertake a more costly deep retrofit,” said Clare O’Connor, the charity’s energy policy officer.

But she said there was scope to better target families on lower incomes “by following the lead of the Dutch government, which offers a zero-interest retrofit loan for households with an income under €60,000″. It also wants the Warmer Homes Scheme, which offers free energy upgrades to people on certain welfare payments and living in properties built before 2006, to be expanded to include HAP tenants and those on disability allowance.

You can contact us at OnTheMoney@irishtimes.com with personal finance questions you would like to see us address. If you missed last week’s newsletter, on how to complain effectively, you can read it here.