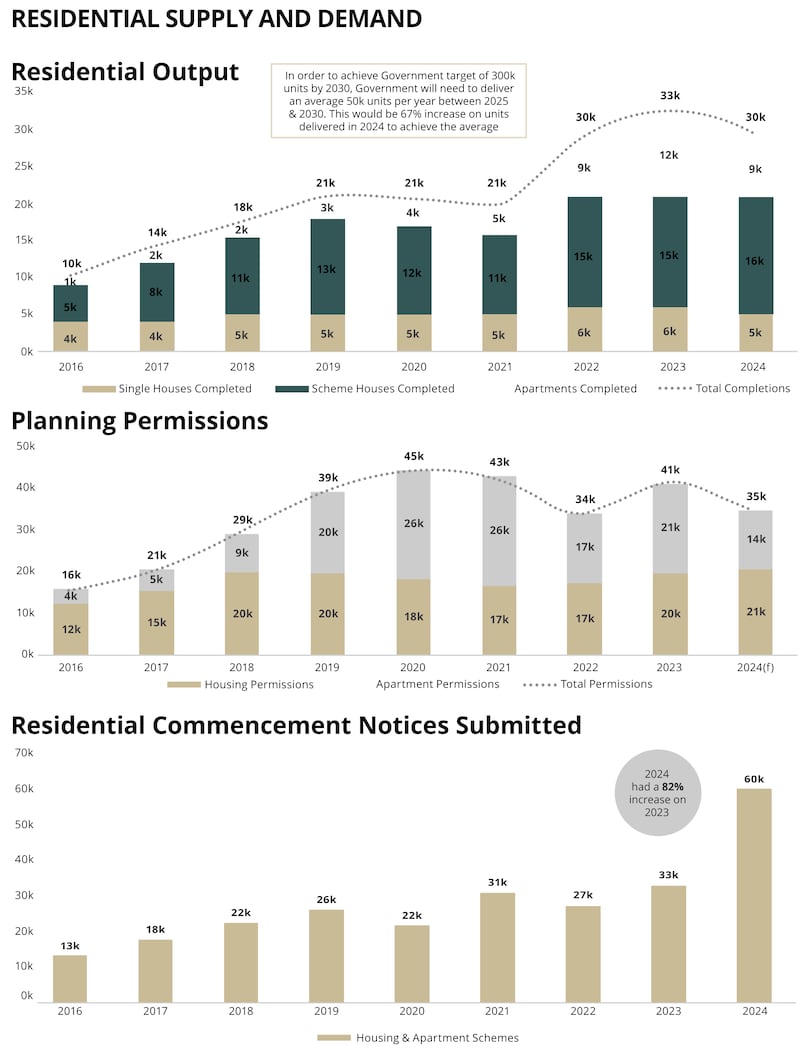

The new Government got two pieces of bad news on housing in its first days in office. The first were figures showing that housing completions last year were 30,330, well below the close to 40,000 that senior ministers had forecast during the election campaign despite analysts saying this was not possible.

Perhaps more worryingly for the new administration was a report by construction consultancy Mitchell McDermott that said this may only rise to 32,000 this year, a more pessimistic view than other forecasters.

Its report warned that delivery is stagnating and “we are going back to 2022”. In separate predictions this week, Goodbody analyst Dermot O’Leary was only marginally more optimistic, predicting 34,000 completions this year.

Just two weeks ago in its programme for government, the new Coalition said it planned to build 300,000 homes by the end of 2030. This was adopting targets set by the outgoing administration last November, which involved an average of 50,500 new homes each year. The target for this year was set then at 41,000.

RM Block

With separate data from the Banking and Payments Federation showing a record number of first-time buyer mortgages and interest rates firmly on the way down, this mix of insufficient supply and strong demand points to prices continuing to rise – and rise.

The supply dilemma

The 2024 figures were embarrassing for the outgoing government. But they had hoped that this year would be better. There was a sharp rise in housing commencements notices lodged by builders last year, which came to 60,000.

This was influenced by waivers on development levies and rebates on water charges available on houses that were commenced before the end of the year. These offer significant savings to builders if they can finish the homes by the end of 2026. The rise in commencements had led to some hope of an increase in completions this year.

Not so, says Mitchell McDermott. It says the more important figure to look at is the number of planning permissions, with 35,000 granted last year, one of the lowest figures over the last six years and down from 41,000 in 2023.

According to Paul Mitchell of Mitchell McDermott, “the reality is that while a developer may put in a commencement notice for 400 units, they might only commence 50 or 100. They wanted to ensure that they would be eligible for granted waivers for the maximum number of units they commenced, but there is no penalty if they commence less.”

And so this Government finds itself facing the same dilemma as the last one – setting a target over which it only has partial control via State-supported programmes, and relying on unpredictable private sector delivery, which it is trying to influence.

The blockages

The Government is pumping billions into housing – so why is output not increasing? The familiar blockages are still there in planning and financing. And a key issue highlighted by the 2024 figures was the fall-off in apartment completions.

The recent Central Statistics Office figures showed 8,763 apartments completed in 2024, down 24 per cent from 2023. The news was a bit better in housing scheme completions, up 4.6 per cent to 16,200 while there was a 2.2 per cent fall in once-off housing completions to 5,367.

The finances of apartment building have long appeared problematic and, more recently, overseas investors reduced their funding sharply as interest rates rose. Even though rates are now on the way down, they are still slow to return. Lobby groups blame the costs of construction here, which is particularly high for apartments, planning and infrastructure delays, and the rental caps which limit returns.

A year of thoughts on Ireland’s housing crisis

Paul Mitchell says previous government policy is at fault, including a change in regulations in December 2022 that meant build-to-rent developments were no longer permitted as a category under planning.

“The introduction of rent caps and the way they were introduced was the final straw for a lot of the international funds, who have taken business elsewhere,” he said.

This is a politically difficult area, with controversy over the tax treatment given to so-called “vulture funds” in the wake of the financial crash and successive governments moving to protect renters from significant increases.

Mitchell estimates that as international funds withdrew, State funding replaced it to some extent via the Land Development Agency, local authorities, Approved Housing Bodies and a variety of support schemes helping developers to finish projects. Without these between 10,000 and 15,000 units would not have been built, he estimates.

The policy issue for the Government and new Minister for Housing, James Browne, is how to attract longer-term international funds to continue to invest in apartment building here and how to marry this with State provision to increase affordability through cost rental and social provision.

[ Housing delivery predicted to stagnate and fall well short of targetsOpens in new window ]

The Commission on Housing had suggestions here, including a detailed analysis on the viability challenges facing denser apartment developments and the financing and planning challenges and proposals on an amended rental cap. For international investors, policy certainty is key.

The Mitchell McDermott report also points to the much-discussed planning delays and the “high mortality rate” for housing schemes. Fast-track planning applications for 200,000 housing units were submitted over the last six years, it says, but just 40 per cent have commenced or are constructed.

These include applications under the now defunct Strategic Housing Development programme and the Large-scale Residential Development programme, which has replaced it, and is working more efficiently. Some 112,000 of the 200,000 units got what the consultants called “usable permission” but even then many of these did not progress.

The Government will hope the new Planning Act will improve things – and is working on a new national planning framework that may change planning guidelines but is not due until the summer. In the meantime, the Government will quickly come under pressure to clear more immediate blockages and point a direction to increasing supply.

House buyers

What about those in the market to buy? Most analysts believe the mix of poor supply and high demand will mean prices will continue to head higher, with the only debate being whether affordability constraints will slow the rate of increase.

Meanwhile, figures this week from the Banking and Payments Federation Ireland show the first-time buyer market is booming, with approvals for this group late last year running at new record highs.

Many of those approved, however, will have difficulty finding a property, and if they succeed they will have to pay up. According to mortgage broker Michael Dowling: “with a dire shortage of second-hand stock for sale (just 0.65 per cent) and Ireland not building enough new homes, first-time buyers are paying more because of lack of supply.

“First-time buyers are outbidding each other in a desperate situation which will see prices continue to rise in 2025.”

John Fahy of brokers Pangaea points out that new buyers are increasingly finding themselves in competition with approved housing bodies (AHBs) in bidding on new homes as the AHBs move to increase supply of social and affordable homes.

It is part of the complex web of questions and trade-offs facing housing policy as attempts are made to increase supply in all different parts of the market. For buyers, Fahy feels prices may go up another 10 per cent this year. Some other forecasts feel affordability constraints could lead to a price increase figure closer to 5 per cent.

Either way, all expect prices to remain on the up, due in part to the continued availability of the State demand support schemes and promises in the programme for government to expand them.

First-time buyers do not look as exposed as they did in the run-up to the financial crash, though those availing of the First Home Scheme need to consider carefully the implications and future costs of the State equity stake in their home, which is part of this arrangement.

And with higher and higher mortgages being taken on, typically the continuation of two incomes at current or rising levels will be required for most borrowers.

The risk is of any wobble in the Irish jobs market in a situation where the ESRI has calculated that house prices are overvalued by 10 per cent or more, creating risks of a painful correction if wider economic trouble hits.