There was good news for the self-employed in this month’s Budget; but maybe not as good as some had hoped. Yes, efforts were made to reach the goal of tax equalisation between those who work for themselves, and those who get paid through the PAYE system with the introduction of a new €550 tax credit, but discrepancies, such as the 3 per cent levy on self-employed income over €100,000 remain.

Sinéad Doherty, managing partner at tax advisers Fenero, welcomes the new tax credit, but was disappointed that the budget didn't do more. "I'm not sure there's a huge amount in it that will help the SME type of self-employed person," she says. "There is still not equality in the tax system."

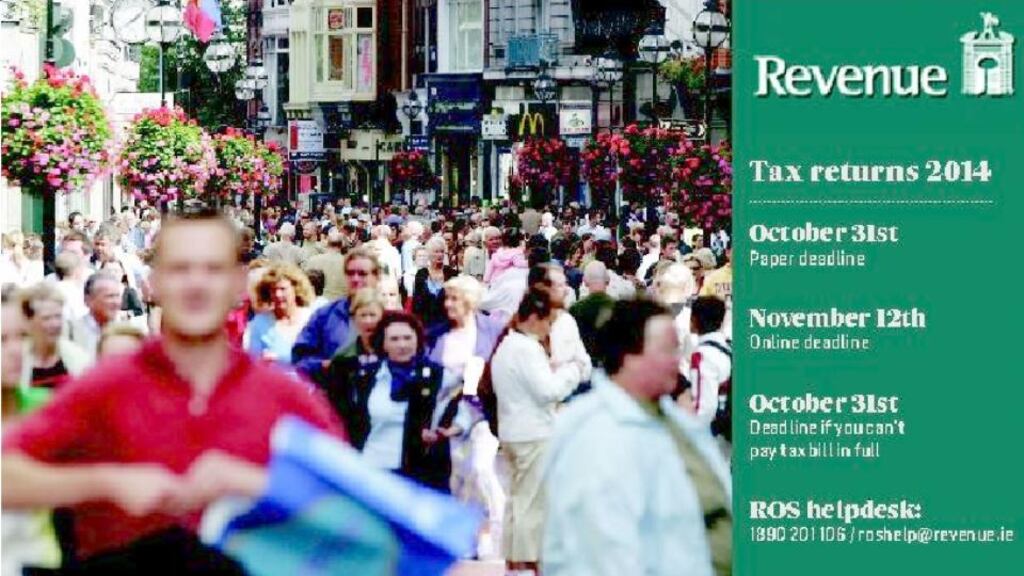

Of course, if you are under pressure trying to meet the upcoming deadlines for 2014 returns, you may not as yet be too concerned about measures that will only make a difference when you file your 2016 return.

One nugget from Budget 2016 that may be of interest however, is the fact that the Revenue Commissioners have been allocated an additional €75 million “for increased audit and investigation activities”. This, it is hoped, will lead to “improved compliance”. So, if you fear that some of this allocation may be spent investigating your taxes, it’s best to get your affairs in order.

What impact will Budget 2016 have?

The main measure introduced in the budget which is of interest to people who work for themselves is the “earned income credit” of €550, which is set to cost the Exchequer about €61 million a year.

Introduced ostensibly to narrow the gap between the self-employed and PAYE employees who receive a credit of €1,650, the credit will help people to cut their tax bill by €550 every year.

If you have a mix of earnings and already benefit from the PAYE tax credit, you won’t benefit from the new measure, as under Revenue guidelines, “the combined tax credits cannot exceed €1,650”.

"You only get one credit – if you've two PAYE jobs for example, [you] only get the PAYE credit once," says Cathal Maxwell of Paylesstax.

Watch out landlords however. The credit is applicable only to trading or professional income – not so-called “unearned” income such as that derived from rents.

And it will take some time for many people to benefit from the new credit, given that it will only come into play in January 2016 – and you won’t file your 2016 tax return until October/November 2017.

But, as Doherty points out, company directors will get a boost to their cash flow much sooner. “Company directors who take a salary as normal like employees and pay their taxes every month will feel the benefit of the credit from January.”

Will self-assessed people see any benefit from previous budgets in this year’s returns?

Not yet unfortunately. Indeed looking back, 2014 can now be seen as the last year of austerity.

To see this clearly, take a look at our case study from our recent “Budget families” series (see http://iti.ms/1LKUPsZ). In 2014 Sam, our self-employed executive, saw no increase in his take-home income of €7,955 a month – and no decrease either. But, this year his net income rose to €8,010 and next year he will see his after-tax income increase again slightly to €8,131.

However, when it comes to paying your preliminary tax for 2015, you could avail of the new lower 40 per cent top rate of tax, if applicable, by opting to pay 90 per cent of your 2015 bill now.

Typically, when paying preliminary tax, you can decide to pay 100 per cent of your 2014 bill, or 90 per cent of your 2015 bill. Given the slight tax change, the latter might be the preferred option, but as Doherty warns, you might find it difficult to estimate your total tax bill with a couple of months still to run in the year.

“If you get that wrong and you underestimate how much you owe, you could be liable for interest charges on the balance,” she warns.

What’s new for 2014?

One big change for those filing returns for 2014 – and who are not self-employed – is the introduction of PRSI at a rate of 4 per cent on “unearned” income.

First signalled back in 2012, this measure is finally coming to pass, and applies to unearned income from January 1st 2014. Self-employed people have already been paying this additional tax.

"Unearned income for everyone else will become subject to PRSI in 2014. This means that PRSI will be payable on income generated from wealth such as rental income, investment income, dividends and interest on deposits and savings," Minister for Finance Michael Noonan said discussing the measure back in Budget 2013.

There are some exceptions however. Firstly, if you are over 66 you are typically exempt from PRSI, which means that you won’t be liable to this.

Remember however that PRSI is calculated separately in respect of each spouse. According to Revenue, this means that if one spouse is over 66, they won’t be liable to PRSI, but if the other is less than this, they will be caught by the new charge.

Secondly, if you are not deemed to be a “chargeable” person by Revenue, you won’t be caught by PRSI.

To avoid this, your total unearned earnings, derived from rental income or interest on deposits etc, should not exceed €3,174 a year.

When it comes to rental income, remember that it’s your profit, rather than total earnings, which are important. So, if you have total rental income of €5,000, but a “profit” of just €3,000, you won’t have to account for PRSI.

Everyone else however – and this means many so-called “accidental” landlords, particularly in the Dublin area – will have to pay an extra 4 per cent in taxes this year.

So, if you are a landlord for example, and you have taxable income of €10,000 from your property, you’ll have to pay an extra €400 in taxes this year. Savings of €160,000 in savings earning interest at 2 per cent would also put you in this category, with interest of about €3,229 a year.

An additional 4 per cent on DIRT of 41 per cent, would see a total tax bill of €1,453 – which doesn’t leave you with much of a return on your savings.

How can I pay the new PRSI charge?

If you are deemed by Revenue to be a so-called “chargeable person”, you must submit a Form 11 every October/ November just like every other self-assessed person.

Typically, this means paying your 2014 tax bill in the following year.

“Any non-PAYE income is always on a year prior basis,” says Maxwell.

If you earn rental income, you will be well used to this, but if you haven’t been subject to the PRSI charge up until now, you may not realise that you should be declaring this income, so may need to familiarise yourself with this form.

“People may have forgotten about it,” notes Maxwell.

And, as self-assessed tax returns also require a preliminary tax payment, this means that if you haven’t already paid this additional charge, you may be subject to interest for late payment.

“PRSI is collected as tax within the self-assessment system so any PRSI due for 2014 should have been considered in making the preliminary tax payment for 2014 by 31 October 2014,” a spokeswoman for Revenue says, noting that the balance – as well as preliminary tax for 2015 – is now due shortly.

“Interest will only arise where the preliminary tax is outside the allowed parameters,” she says.

Rather than sending in a cheque, PAYE taxpayers may find that the Revenue will adjust your tax credits and collect the tax this way. Property tax Is it deductible yet? Uncertainty over whether or not property tax is deemed to be a deductible expense in income tax returns has long been a source of frustration for some, and a bone of contention for others. But the issue now seems to be drawing to a conclusion – just not a favourable one for landlords.

In the original Thornhill Report on property tax penned for the Department of Finance by Dr Don Thornhill, it was suggested that property tax should be treated as a deductible expense. The Government responded in kind, by asserting that it would be phased in over a number of years. Until then, landlords were advised by the Revenue that "LPT is not a deductible expense and therefore should not be claimed as a deduction".

Last Tuesday however, the Department of Finance published an updated report from Mr Thornill. And, “after further reflection”, Mr Thornhill now finds that it would be “inappropriate” to allow landlords to offset the tax against their income tax returns. “LPT should not be allowed as a deduction in computing net profits from the letting of residential properties for income and corporation tax purposes,” he wrote, arguing that on “conceptual and equity grounds” it wouldn’t be appropriate that they should do so. “Owner occupiers are not allowed to claim LPT as a deduction against income tax.”